How I Protect My Biggest Investment—My Home, the Smart Way

What if everything you’ve built could vanish overnight? I learned the hard way that owning property isn’t just about pride—it’s about protection. After a surprise storm damaged my roof, I realized my savings were at risk too. That’s when I dug into property insurance, not as a formality, but as a real shield for my assets. This is how I turned a scary moment into a smart strategy—one that could save you from financial disaster. What started as a stressful repair bill became a wake-up call about the true cost of being unprepared. Now, I see insurance not as an unavoidable expense, but as a critical component of financial security. This is the story of how I took control of my home’s protection—and how you can too.

The Wake-Up Call: When My House Became a Liability

It started with a storm—one that wasn’t even forecasted as severe. By morning, half of my roof was gone, shingles scattered across the yard like fallen leaves. The damage seemed contained at first, but the estimate from the contractor told a different story: over $28,000 to repair and reinforce. I had savings, but not that much set aside for emergencies. More alarming was the realization that without proper insurance, this single event could drain my financial reserves and threaten my long-term stability. I had assumed my standard policy would cover it. I was wrong.

This moment shifted my understanding of homeownership. I’d always thought of my house as an asset—something that appreciated, provided shelter, and symbolized success. But without protection, it quickly became a liability. The emotional toll was just as heavy as the financial one. I felt exposed, frustrated, and misled by my own assumptions. I’d paid premiums for years, yet now, when I needed support most, the coverage fell short. It wasn’t that the insurance failed me; it was that I had never taken the time to understand what it actually covered. That gap in knowledge nearly cost me everything.

What I learned is that many homeowners operate under the same misconception: that having a policy is the same as being protected. But insurance is only effective when it’s properly aligned with your home’s real value and the risks it faces. For me, the storm wasn’t just an act of nature—it was a test of preparedness. And I had failed. The good news? That failure became the foundation for a smarter, more intentional approach to protecting my investment. I began researching, asking questions, and comparing policies not just for price, but for true value. What emerged was a strategy focused not on avoiding premiums, but on maximizing protection.

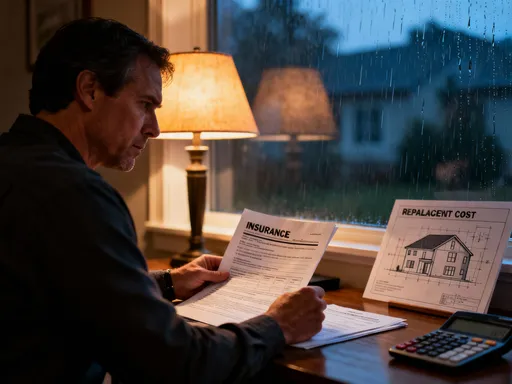

What Property Insurance Really Does (And What It Doesn’t)

Most homeowners assume their property insurance is a safety net for any kind of damage. In reality, it’s a carefully structured agreement with defined limits and exclusions. At its core, a standard homeowners policy typically includes four main components: dwelling coverage, personal property protection, liability insurance, and additional living expenses. Dwelling coverage pays to repair or rebuild the physical structure of your home if it’s damaged by a covered peril, such as fire, wind, or hail. Personal property coverage helps replace belongings lost in a covered event, from furniture to electronics. Liability protection kicks in if someone is injured on your property and you’re found responsible. Additional living expenses cover temporary housing and meals if your home becomes uninhabitable during repairs.

But here’s what many don’t realize: not all risks are covered. Standard policies routinely exclude damage from floods, earthquakes, and sewer backups. Wear and tear, mold from long-term moisture, and damage caused by pests are also typically excluded. These exclusions exist because insurers consider them either predictable or preventable, not sudden or accidental. Yet for homeowners, these are often the very risks that cause the most expensive and disruptive damage. I discovered this the hard way when my claim for water damage was partially denied because the source was traced to a slow leak that had gone unnoticed for months—a classic case of wear and tear.

Understanding what your policy does and doesn’t cover is essential to avoiding financial shock. Many people only read the fine print after a claim is denied, but by then, it’s too late. The key is to review your policy annually, ask your agent to explain exclusions in plain language, and assess whether your current coverage matches your home’s actual risks. For example, if you live in a region prone to heavy rainfall, water backup coverage might be critical. If you’re near fault lines, earthquake insurance may be worth considering. Recognizing these gaps allows you to make informed decisions about supplemental protection.

Why Standard Policies Aren’t Enough for Real Asset Preservation

While a standard homeowners policy may satisfy your mortgage lender’s requirements, it often falls short when it comes to truly preserving your wealth. Lenders care that the structure has basic coverage, but they don’t ensure that the amount is sufficient to rebuild your home to current standards. This is where the concept of underinsurance becomes dangerous. Many policies are based on outdated valuations or market prices, which don’t reflect the actual cost of construction materials, labor, or code upgrades after a disaster. As a result, homeowners can find themselves with a $400,000 policy on a home that would cost $550,000 to rebuild—leaving a $150,000 gap they must cover themselves.

Another overlooked issue is the rising cost of building materials and skilled labor. Over the past decade, construction prices have increased significantly due to supply chain issues, inflation, and labor shortages. A roof that cost $15,000 to install ten years ago might now cost $28,000 or more. If your policy hasn’t been adjusted to reflect these changes, you’re effectively underinsured. Similarly, home improvements like kitchen remodels, solar panel installations, or finished basements often aren’t automatically included in your coverage. Without updating your policy, these upgrades represent uninsured assets—money invested that isn’t protected.

The goal of insurance shouldn’t be just to meet minimum requirements, but to ensure long-term financial resilience. A policy that barely covers the structure isn’t preserving your asset—it’s offering false security. Real asset preservation means aligning your coverage with the true cost of rebuilding, including inflation protection and coverage for improvements. This requires proactive management, not passive acceptance of whatever policy you were given at closing. It’s the difference between having insurance and having meaningful protection.

Upgrading Your Shield: Riders, Endorsements, and Extended Coverage

Once I understood the limitations of my standard policy, I began exploring ways to strengthen it. The solution wasn’t switching insurers, but enhancing my existing coverage through riders and endorsements—optional additions that expand protection for specific risks. These upgrades may cost slightly more in premiums, but they offer disproportionate value when disaster strikes. One of the first I added was guaranteed replacement cost coverage. Unlike standard policies that cap payouts, this endorsement ensures the insurer will pay whatever it takes to rebuild your home, even if costs exceed the policy limit. Given the volatility of construction prices, this single addition provided immense peace of mind.

I also scheduled high-value items like jewelry, fine art, and electronics. Standard personal property coverage often has sub-limits for categories like jewelry or collectibles—sometimes as low as $1,500. If you own a $10,000 engagement ring or a rare painting, that limit won’t come close to covering replacement. By scheduling these items, I ensured they were covered for their full appraised value, regardless of the overall policy cap. The process was simple: I provided receipts and appraisals, paid a small additional premium, and gained specific protection for my most valuable possessions.

Another critical upgrade was water backup and sump pump overflow coverage. This endorsement protects against damage caused by sewage or water backing up into your home—a surprisingly common and costly issue, especially in basements. While not included in standard policies, it’s available for a modest increase in premium. I also added ordinance or law coverage, which pays for upgrades required by current building codes during reconstruction. For example, if your old wiring needs to be replaced with modern code-compliant systems, this coverage helps cover the added expense. These enhancements transformed my policy from a basic safety net into a comprehensive shield.

The Hidden Risk: Underinsurance and How to Avoid It

Underinsurance is one of the most widespread yet invisible risks in homeownership. It occurs when your coverage amount is less than the cost to rebuild your home. Many people confuse market value with replacement cost, but they are not the same. Market value includes land, location, and local demand—factors that don’t affect rebuilding costs. Replacement cost, on the other hand, is the actual expense of reconstructing your home from the ground up, using current materials and labor rates. A home valued at $600,000 on the market might only have a land value of $150,000, meaning the structure itself could cost $450,000 or more to rebuild.

To avoid underinsurance, start by obtaining a professional replacement cost estimate. Many insurers provide this during policy issuance, but it’s wise to verify it independently. You can work with a local contractor, use online builder cost calculators, or hire a certified appraiser. Be sure the estimate includes not just the main structure, but also detached buildings, driveways, and landscaping features that would need reconstruction. Also, consider inflation protection or extended replacement cost coverage, which automatically adjusts your limit to keep pace with rising construction costs.

Another step is to document all home improvements. Whether you’ve added a deck, upgraded your HVAC system, or remodeled the kitchen, these changes increase your home’s replacement value. Inform your insurer and request a policy adjustment to reflect these upgrades. Keeping detailed records—receipts, permits, photos—makes this process easier. Finally, review your policy annually, especially after major life events like renovations or inflation spikes. Underinsurance isn’t a one-time mistake; it’s a condition that can develop over time if you’re not vigilant. Staying proactive ensures your coverage keeps pace with your investment.

Shopping Smarter: How to Compare Policies Without Getting Played

When it comes to choosing or renewing your homeowners insurance, the lowest premium isn’t always the best deal. In fact, focusing solely on price can lead to inadequate coverage and costly surprises down the road. Smart shopping means evaluating policies based on value, not just cost. Start by comparing coverage limits, not just dollar amounts. Two policies may both offer $400,000 in dwelling coverage, but one might include guaranteed replacement cost while the other doesn’t. That difference could save or cost you tens of thousands in a claim.

Deductibles are another area where small differences matter. A higher deductible lowers your premium, but it also means you’ll pay more out of pocket when you file a claim. Consider your emergency fund: can you afford a $5,000 deductible if disaster strikes? For many families, a $1,000 or $2,500 deductible is more realistic. Balance affordability with financial safety. Also, look at how each insurer handles claims. A company with a low premium but a history of slow or denied claims may not be worth the savings. Check customer satisfaction ratings from sources like J.D. Power or the National Association of Insurance Commissioners to gauge reliability.

Don’t hesitate to ask questions. What is the claims process like? How quickly do adjusters respond? Are there discounts for safety features like security systems or storm shutters? Does the company offer multi-policy bundling? Transparency matters. A reputable insurer will explain coverage clearly, disclose exclusions upfront, and help you understand your options. Finally, get quotes from at least three providers every few years. Loyalty is valuable, but the market changes, and new competitors may offer better terms. Regular comparison keeps you informed and in control.

Making It Work: Habits That Keep Your Protection Active and Effective

Insurance isn’t a set-it-and-forget-it decision. To remain effective, it requires ongoing attention and routine maintenance. One of the most powerful habits is the annual policy review. Set a reminder each year to go through your coverage, check for changes in value or risk, and confirm that all endorsements are still active. This simple step can prevent coverage gaps caused by inflation, renovations, or life changes. It’s also an opportunity to reassess your deductible, update your inventory, and ask about new discounts.

Another essential practice is maintaining a detailed home inventory. This list of your belongings, complete with photos, receipts, and estimated values, is invaluable if you ever need to file a claim. Store it in a secure cloud account or external drive so it’s accessible even if your home is damaged. Update it every time you make a significant purchase or complete a home project. This habit not only speeds up claims but also helps you determine if your personal property coverage is adequate.

Finally, communicate with your insurer about life changes. Moving, renting out a room, running a home-based business, or even getting a pet can affect your coverage needs. Some changes may require additional liability protection or a separate policy. Staying in touch ensures your policy evolves with your life, not falls behind it. These small, consistent actions transform insurance from a passive expense into an active tool for financial security.

Protecting More Than a House—Safeguarding Your Future

Your home is more than walls and a roof. It’s a repository of memories, a haven for your family, and one of the most significant financial investments you’ll ever make. Treating property insurance as a mandatory cost misses its true potential. When approached strategically, it becomes a powerful mechanism for preserving wealth, avoiding debt, and maintaining stability in the face of uncertainty. The storm that damaged my roof could have derailed my financial plans, but instead, it led me to a deeper understanding of protection.

Smart insurance isn’t about fear—it’s about foresight. It’s recognizing that risk is inevitable, but financial disaster isn’t. By understanding your policy, closing coverage gaps, and maintaining active oversight, you turn a basic contract into a personalized defense system. You protect not just your home, but your savings, your peace of mind, and your future. In the end, the most valuable thing you can insure isn’t the structure itself—it’s the life you’ve built inside it.